Old Pension Scheme (OPS) and New Pension Scheme (NPS) Key Differences, Pension Amount, Eligibility & Benefits Explained (2025 Guide)

Many government employees in India are comparing the Old Pension Scheme (OPS) with the New Pension Scheme (NPS) because both plans give financial support after retirement. Some states have already shifted back to OPS, which has restarted the national debate on which system is truly better for long-term stability.

Both schemes aim to provide security after retirement, but they follow very different methods. OPS promises a fixed pension for life, while NPS builds a retirement fund through employee and government contributions. These differences affect monthly income, tax benefits, and long-term planning.

To help you understand the real picture, this article explains both schemes in simple, easy-to-read language with clear examples, updated details, and unbiased comparison.

Understanding the Old Pension Scheme (OPS)

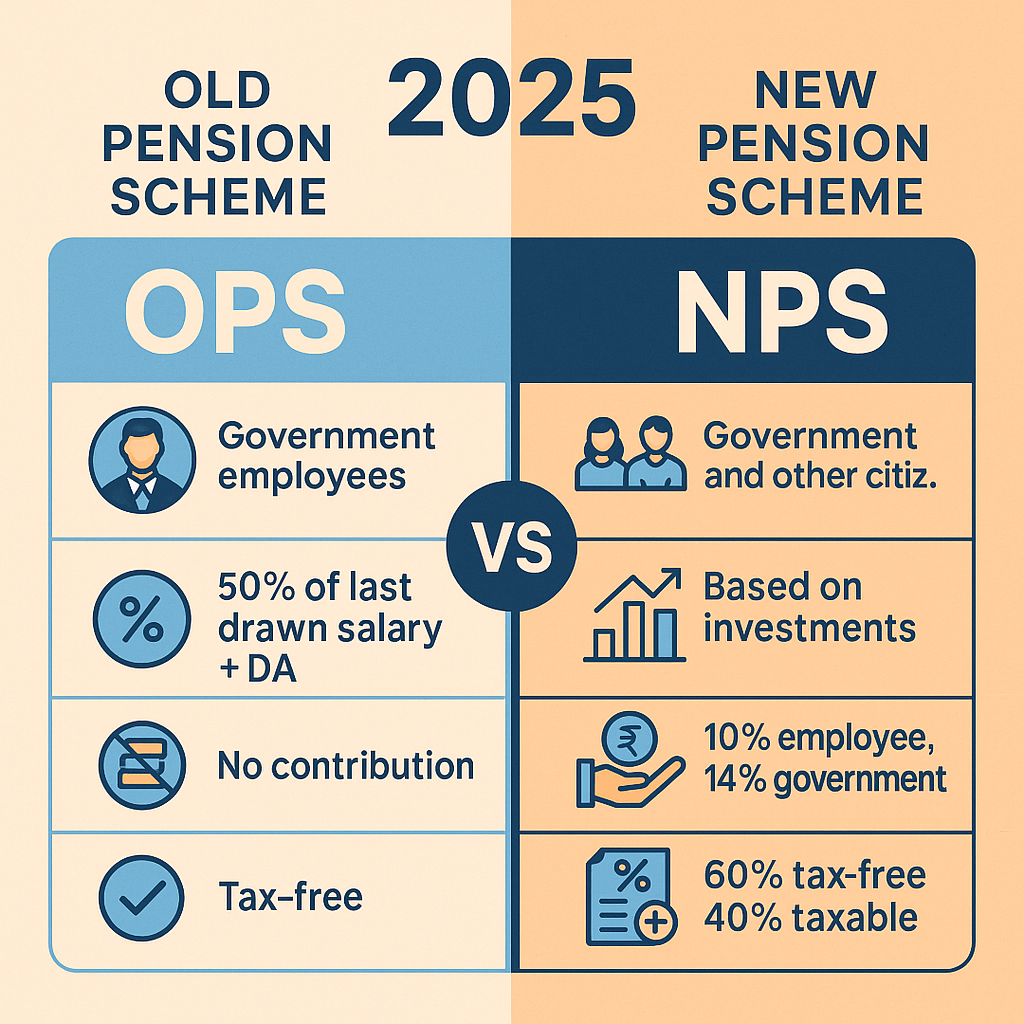

The Old Pension Scheme guarantees a fixed monthly income after retirement. Under OPS, an employee receives 50% of the last drawn basic salary plus Dearness Allowance (DA), or the average monthly salary of the last 10 months—whichever gives a better pension. This formula makes OPS stable and predictable.

Unlike NPS, employees do not contribute any amount from their salary. The entire payment is made by the government. Pension automatically increases when DA is revised two times every year, which helps retired employees deal with rising prices.

OPS is available only for government employees. Private workers and self-employed individuals cannot join this scheme. It was stopped for new central government employees in 2004, but some states later restored it for their workers.

Who Received the Option to Shift Back to OPS?

In February 2023, the Department of Pension and Pensioner’s Welfare (DoPPW) allowed some central government employees to switch from NPS to OPS. This was a one-time window given with strict conditions.

Employees could shift to OPS only if they:

- Joined service on or after 1 January 2004

- Were selected for a post advertised before 22 December 2003

- Were currently part of NPS

Applications had to be submitted before 31 August 2023. Anyone who missed the deadline continues under NPS.

Benefits and Limitations of OPS

Key Benefits

- Predictable monthly pension for life

- Pension grows twice a year through DA revisions

- No compulsory employee contribution

- Full financial responsibility handled by the government

- Family pension is available to the spouse after the employee’s death

Key Limitations

- High financial cost for the government

- No pension fund is created for future returns

- Long-term sustainability is difficult because life expectancy is increasing

- Pension bills rise every year, which puts pressure on state budgets

How the National Pension Scheme (NPS) Works

The National Pension Scheme (NPS) was introduced in 2004 to control rising pension expenses. It works as a contribution-based system where both government and employees deposit money every month.

Government employees contribute 10% of their basic pay plus DA, while the government contributes 14%. The amount is invested in equity, bonds, and government securities by professional fund managers such as SBI, LIC, and UTI. Returns depend on market performance but are regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

At retirement (age 60), subscribers can withdraw up to 60% of the accumulated fund tax-free. The remaining 40% must be used to buy an annuity, which pays monthly pension.

NPS is open to everyone—government employees, private-sector workers, self-employed individuals, and NRIs—making it a wider retirement option than OPS.

Why NPS Is Considered a Modern Pension Model

NPS builds a retirement corpus over time. This corpus grows with investment returns, making it suitable for a growing economy. PFRDA monitors fund managers, investment rules, and performance to ensure transparency.

Subscribers can change their fund manager, shift between equity and debt, and even make partial withdrawals after 10 years for personal needs. The scheme is fully digital, allowing contributions and tracking through online portals.

NPS also offers strong tax benefits, including an extra deduction of ₹50,000 under Section 80CCD (1B), which is over and above the ₹1.5 lakh limit under Section 80C.

Major Differences Between OPS and NPS

| Feature | Old Pension Scheme (OPS) | National Pension Scheme (NPS) |

|---|---|---|

| Who Can Join | Only government employees | All citizens aged 18–60, including NRIs |

| Pension Calculation | 50% of last basic pay + DA | Based on accumulated fund and annuity rate |

| Employee Contribution | No contribution | 10% of salary (basic + DA) |

| Government Contribution | Not applicable | 14% of employee salary |

| Tax Benefits | No tax benefits | Deductions under 80C and 80CCD(1B) |

| Tax on Final Amount | Pension is tax-free | 60% fund tax-free, 40% taxable through annuity |

| Risk | No risk | Market-linked returns |

| Inflation Protection | Automatic DA hikes | Depends on annuity plan |

Is OPS or NPS Better for Employees?

OPS provides stability because the pension amount is fixed. If a government employee retires with a basic salary + DA of ₹10,000, the guaranteed pension becomes ₹5,000 per month. When DA increases by 4%, the pension rises to ₹5,200. This system protects the employee from inflation.

NPS works differently. It depends on the total contributions and the investment return. For example, if an employee begins at age 35 and continues until 60, with monthly contributions of ₹2,400 (₹1,000 employee + ₹1,400 government), the accumulated value can provide both a lump sum and a pension.

NPS gives flexibility, better tax savings, and market-linked growth. It also reduces pressure on the government budget. For long-term sustainability, experts believe NPS is more practical for the economy.

Why Governments Prefer NPS for the Future

With rising life expectancy and frequent pay revisions, pension payments under OPS continue for decades. This makes OPS difficult to maintain for state and central governments.

NPS shares the responsibility between the government and employees and uses investment growth instead of a direct payout model. This approach helps control government expenditure while still supporting employees through a combination of pension and lump-sum benefits.

Frequently Asked Questions (FAQs)

No. OPS is not available for new central government hires after 1 January 2004.

Yes. After 10 years of opening the NPS account, subscribers can make partial withdrawals for reasons such as education, medical treatment, or home purchase.

The amount depends on total contributions, investment returns, and the annuity plan chosen. Typically, subscribers receive a monthly pension plus a tax-free lump sum.

No. OPS does not provide tax deductions for employees during their working years.

OPS gives a fixed pension linked to last salary and DA. NPS can give higher returns over the long term, but the pension is not fixed and depends on market performance.